New Closing Disclosure Rules

On November 20, 2013 the CFPB announced the completion of their new integrated mortgage disclosure forms along with their regulations (RESPA Regulation X and TILA Regulation Z) for the proper completion and timely delivery to the consumer. These regulations are known as “The Rule”.

Any residential loan originated after October 3, 2015 will be subject to the new rules and forms set forth by the CFPB*. The Rule replaces the Good Faith Estimate (GFE) and early TILA form with the new Loan Estimate. It also replaces the HUD-1 Settlement Statement and final TILA form with the new Closing Disclosure. The introduction of the new disclosure forms requires changes to the systems that produce the closing forms. Fidelity National Title Group is already well underway in preparing our production systems to provide the new required fee quotes, prepare the new closing disclosure forms, and track the delivery and waiting periods required by the new regulations.

*Loans in progress (applications submitted prior to October 3, 2015) will use current TILA and RESPA forms.

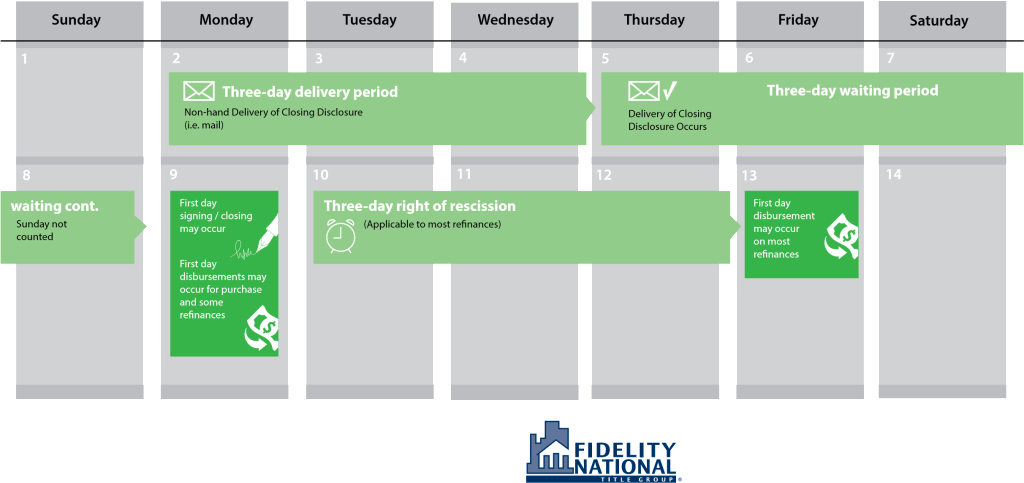

CHANGES TO THE CLOSING DISCLOSURE TIMING

In addition to new forms for residential mortgage transactions, the new regulations also require delivery timetables for delivery to consumers, impacting when a closing can take place and disbursements made. Below is a preview of how the CFPB regulations will impact the closing process for transactions that originate after October 3, 2015.

* As of October 3, 2015 for residential purchase and refinance transactions.